As a frequent blog reader I often run across articles with some form of title such as "7 Secrets of ....." or "10 Tips For ..." and my reaction is always "How do we know there are only 7 secrets?" or "Are there really just 10 tips someone can use?"

Sometimes these figures can represent nothing more than the number of things the author was able to come up with as they were writing their article!

In order to get past these limitations, I like to employ a technique I call triangulation (not to be confused with land surveys).

Triangulation is a process we have used in prior posts (Triangulating Mission and Vision Using Mind Maps and Triangulating Steve Jobs for example). The method consists of two steps:

- gather together a number of different sources of information about a topic we are concerned about, and

- for each source, identify areas of similarity and difference with the others

We can picture this process with the Venn diagram shown in Figure A. Each circle represents one perspective on the topic, such as Author A's "7 Secrets" or Author B's "10 Tips". Researching a topic in this manner creates two useful classes of information.

First, we are able to identify elements that have a universal commonality. The star in Figure A shows the area where all agree - i.e. one of Author A's "Secrets" is also one of Author B's "Tips".

Second, we are able to expand the size and scope of our information base. Keeping the math simple, if each of 5 authors has 10 "Secrets" or "Tips", and 5 are common to all the authors and none of the others overlap, then we end up with 55 "Secrets" or "Tips" rather than 10!

The benefit to the first approach is that we get to focus on the most important elements. After all, the items that most or all experts agree are important probably are important, and by identifying what these items are we can focus on them and not get led down blind alleys. In essence we are making use of the 20/80 rule as we consider the issue.

The advantage to the second approach is that we get a more complete representation of the topic - i.e. we have gotten closer to learning all the "Secrets" or "Tips". This larger universe gives us a wider range of potential actions or ideas to pursue, and reduces the chance that we are going to overlook something important.

One technique used to generate innovation ideas is to "split" a concept or problem into two different attributes, then split each of those into two, then each of those into two, and so on until we have a number of pieces that we can rearrange like a puzzle (note - I originally learned this technique from the book "Thinkertoys").

I was practicing this technique recently using the term "CFO". The three initial split possibilities I identified during this exercise were:

- ::Activities and Characteristics

- ::Small Business and Large Business

- ::Public Company and Private Company

In reviewing this list, I recalled that we addressed the "activities" dimension of the first split in the list above last Fall in a post entitled Triangulating the CFO Mission Using Mind Maps but that we have not done much analysis of the "characteristics" path up to this time.

So let's check it out!

The first step in our triangulation process is to identify a number of sources to review. A logical group from which to choose would be the "customers" of the CFO.

One of my favorite representations of the CFO's stakeholders is the CFO Relationship Map by Samuel Dergel, reproduced here in Figure B. In this map he identifies four main vectors of relationship:

- ::Vertical Up - stakeholders the CFO reports to, such as the CEO, Board of Directors, and Investors

- ::Vertical Down - those that report to the CFO

- ::Horizontal External - those outside the organization whom the CFO deals with on a more or less equal footing

- ::Horizontal Internal - those within the organization that are peers, such as other C-level executives

The "Vertical Up" groups - board, investors and CEO - are arguably the most important portion of the relationship map, if for no other reason than it is these folks who sign the CFO's paycheck. If they're not happy, extremely positive relationships in the other three relationship sectors are not likely to matter much.

The most in-depth relationship within this group is the CEO. In "CFOs: Characteristics and Qualities of Top Performers", survey results revealed that half of the CFOs spent 3 hours or more per week with the CEO in 1:1 settings. The study notes that:

"The hallmark characteristic for this relationship is candor, with nearly all of the Top CFOs reporting a strong ability to be direct and candid in communicating with the CEO."

Frank interpersonal exchange is a quality echoed by Kevin Rakin (former CFO, longtime CEO, member of several boards, private investor), who states in CFO Magazine's What Entrepreneurs, VCs Think About CFOs:

"You want a CFO and a CEO who [will] be able to call each other on a Sunday night, talk honestly and hash something through. Investors pick up on that. When you go out on a roadshow they can see whether these guys are a team or are going to have ego fights over whatever’s going on"

James Robinson, co-founder and managing partner of venture-capital firm RRE Ventures, in the same article calls this characteristic "a personality fit with a particular company and its CEO".

Ken Marshall, serial entrepreneuer and current CorrelSense CEO, notes in the CFO Magazine article that the "CFO needs to provide a reality check when the CEO gets into that [driving too fast due to obstacle blindness] mode". In order for this to occur productively, the CFO must engender both trust and respect in their CEO relationship.

Investors also consider the CEO-CFO relationship to be important. The g.a. kraut company published a whitepaper consisting of 11 interviews with investment professionals entitled "What Makes a Great CFO?". One of the professionals interviewed in this article said:

"... it's more than just having a handle on the numbers. In fact, that's the minimum requirement. If the CFO can add value on the operating side or the strategic side, that's when you see the CEO and CFO are running the company together."

While another said:

"It’s very important that the Street understand the relationship between the two because it’s an important piece of the Street having confidence in the CFO.

Figure C shows the tag cloud (produced using Tag Crowd website) for the "What Makes a Great CFO?" article.

Reconfiguring these into a sentence, we might say that the "great" CFO's "Help People (including Investors) Understand the Business and the Company".

The "Help People Understand the Business" and "Partner with the CEO" themes apply to board relations as well. In a blog post from North Carolina State's Poole College of Management's Enterprise Risk Management Initiative entitled "The CFOs Relationship with the Audit Committee for Effective Risk Management", the authors state:

"Audit committees are especially committed to oversight on behalf of shareholders and they expect CFOs to do the same. CFOs that follow CEO-level thinking, in thoroughly understanding the business, have a more powerful impact. The primary objective of a business is to drive intrinsic value- this requires a complete understanding of the company’s environment and the industry’s competitive atmosphere."

The "Horizontal External" groups represent professionals outside the firm with whom which the CFO interacts. These include auditors, lawyers, banks and other major service providers.

This is a broad group, which makes it difficult to generalize. For example, auditors are privvy to all the information the firm produces, whereas many bankers will only be told information that is 'publicly available'.

Arthur F. Rothberg, the Managing Director of CFO Edge (a provider of interim CFO services), in his "Audit Preparation: A Formula for High Return on Audit Investment" whitepaper states "Successful audit preparation and audit completion are deeply grounded in the working relationship between the company and its audit partner", and that the company is the one that "sets the tone" in the relationship, primaily through its level of "honesty" and "integrity".

According to CFO Magazine, in "Auditor Angst", "ask auditors what keeps them awake at night and client-related issues will top their replies." These primary stresses can be generated all along the continuum, from unprepared audits on the one end to "difficult to work with" clients on the other.

Interestingly, the magazine noted that "the hassle from clients, in fact, far outranked other strains, such as the pressure to generate more revenue." At heart, basic relationship issues are at play, such as "consideration", "appreciation", "failing to seek input", "no surprises" and "taking the time to get us what we need".

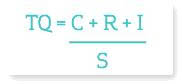

TQ = Trust

C = Credibility

R = Reliability

I = Intimacy

S = Self-Orientation

The groups in the Horizontal External category are advisory - they are supplementing the CFO's core knowledge with deep insight and experience in particular professional niches. One useful depiction of the advisory relationship is Charles H. Green's Trust Equation, which is shown in Figure D.

The equation itself tells us something of what a CFO needs to do. If an advisor is trusted because they are creditible, then the CFO needs to be able to identify creditibility. If an advisor is trusted because of intimacy, then the CFO needs to be intimate.

In the Trust Equation, the level of "self-orientation" of the advisor has a significant impact. The other 3 terms can be overwhelmed if the advisor is "out for themself", while advisors can magnify their trust by maintaining an "other" orientation. The ability to discern between those with an underlying motive and those who are "true friends" is therefore critical in terms of selecting advisors who are truly trustworthy.

The "Horizontal-Internal" and "Vertical-Down" paths share the characteristic that both are part and parcel of the specific organizational context, and for this reason will exhibit similarities.

The internal organization of the firm creates significant relationship opportunities and challenges for the CFO. The size and composition of the "C-Suite" team will determine who the CFO's peers are and what "fiefdoms" they control. Each executive's organizational power and influence will be concentrated if the number of peers is small, while it will be diffused if the team is large.

A CFO must be his/her own worst critic if they are going to continuously grow, develop, and step up their performance. Korn/Ferry, one of the top executive "headhunter" firms, in their "Developing Your C-Suite" whitepaper, discusses the perils CFOs face without this trait:

"C-suite executives often see themselves—rightly so—as among the select few, the special club of those who have reached the top, the best and the brightest. Moreover, family, friends, associates, employees, and the media treat them as though they are the most gifted and accomplished people in their field—the stars of the show, so to speak. This is heady stuff, and it can propel executives into a delusional “fun house” where their self-image is distorted by the success they have attained. If executives believe all the hype about themselves, they can fall prey to two disabling mindsets — the myths of attainment and infallibility."

Others have called this "living in the bubble" (my apologies for not remembering the source).

The "myth of attainment" Korn/Ferry mentions refers to the following mindset:

"Many C-suite executives conclude — consciously or unconsciously — that when they reach this pantheon of business they have “arrived,” and, having reached the top, have nothing more to learn."

While the "myth of infallibility" refers to:

"People who have been successful and made good decisions throughout much of their professional lives can come to believe that they are infallible, and their status as C-suite executives can amplify this effect. Moreover, others in the company often treat them as though they are infallible, which may be more a tribute to their power than a recognition of actual superiority."

Four abilities are helpful in innoculating the CFO from falling prey to these myths:

- ::Contrarian Mindset - the ability to go against the prevailing trend

- ::Social Independence - turning a deaf ear to the expectations and feedback one is receiving from many in the community

- ::Strong Desire to Personally Improve - using internal motivation to determine goals, actions, and priorities

- ::Introspective Capability - the ability to question and examine one's own thoughts and behaviors without prejudice

In addition to the above, Korn/Ferry discuss a more general aspect of the organizational environment they dub the "Captain of the Ship" syndrome:

"...executives live life in a fishbowl. People are watching them constantly and closely, looking for signs of encouragement or danger. After all, when the leader is glum, it may foreshadow doom for everyone else. Conversely, when the leader is relaxed, confident, and happy, it signals good times ahead... "

This implies that:

"Consequently, even if captains of ships or C-suite executives have doubts and uncertainties, even if they know they need help, even if they want more development, they are often reluctant to reveal weaknesses because doing so could sow the seeds of doubt, and with doubt come defections (who wants to remain on a sinking ship?), loss of confidence, and anxieties that get in the way of the real work to be done..."

Finally concluding that:

"The C-suite can be a paralyzing environment for executives who prefer openness and candor."

It is interesting to note that Korn/Ferry brings us to the opposite conclusion we explored earlier in the "Stakeholders Who Pay the Bills" section - which was all about frank conversations, opinions, and "telling it like it is".

Lest we forget, the CFO is also an entity in Dergel's diagram, and perhaps it is the most important one.

We have so far identified a listing of traits required of the CFO from different perspectives. A number of these may "roll-up" under the heading of "Executive Presence", which is a term used to describe the sense we have that a person is capable of work at that level.

Suzanne Bates, CEO of her own communications firm for the past 13 years, in her blog post The 7 Elements of Executive Presence, identifies seven (surprise!) factors that comprise Executive Presence:

- ::Substance - demonstrating command of subject matter and "sharing that expertise in a powerful way". She notes that "if you cannot convey your business and technical skill, you won’t get the recognition you deserve".

- ::Personal Style - the way we dress and conduct ourselves. Bates notes that "Your business attire should make you feel confident and powerful every single day"

- ::Physical Presence - how you project yourself physically, both in action and attitude. Bates says "Learn to sit, stand, walk, move and gesture purposefully - it says so much about your professionalism"

- ::Vocal Skill - monotone speakers do not demonstrate executive presence. Suzanne tells us "your voice should be conversational and clear, and it should demonstrate your confidence, enthusiasm, passion and intelligence"

- ::Manners/Etiquette - showing concern for others comfort, being "gracious", and demonstrating an awareness of the protocols in various situations

- ::Receptivity/Listening - Ms. Bates explains "Listening includes being accessible, encouraging people to express themselves, listening with mindfulness, not speaking too much, and using verbal and non verbal language to convey genuine interest in the other person"

- ::Workspace - the workspace is an "extension of you", and as such it communicates to others messages that can be as powerful as if it came from us directly. Bates notes that our offices "can be a tip off to others about how you really conduct business"

Note that aside from the first item on the list, none of these characteristics have to do with technical expertise as opposed to personal qualities.

Paul Aldo, former professor turned management consultant turned leader developer, in So What is Executive Presence Again? identifies nine "dimensions" that comprise Executive Presence, broken down into three categories:

"Personal Dimensions

::Passion - the expression of motivation,drive, and engagement that convences others you are committed to what you are saying and doing.

::Poise - a look of sophistication and unflappability that creates the impression you are comfortable in your surroundings and able to handle adversity.

::Self-Confidence - the air of optimism and assurance that convinces others you have the required strength, resources, and resolve ti initiate and lead.

Communication Dimensions

::Candor - the appearance of being interested in truth and honesty, with a willingness to accept and engage the world as it is, not as you would like it to be.

::Clarity - the ability to create your story and tell it in an intuitively clear and compelling way.

::Openness - the willingness to consider other points of view without prejudging them.

Relational Dimensions

::Thoughtfulness - the projection of thoughtfulness when dealing with others that conveys an interest in them and the relationship.

::Sincerity - the conviction of believng in and meaning what you say.

::Warmth - the appearance of being accessible to others, physically and emotionally."

D.A. Benton, in her book "Executive Charisma", identifies 6 factors involved:

- ::"Be the First to Initiate"

- ::"Expect and Give Acceptance"

- ::"Ask Questions and Ask Favors"

- ::"Stand Tall, Straight, and Smile"

- ::"Be Human, Humerous and Hands On"

- ::"Slow Down, Shut Up, and Listen"

CFO’s need to make a great first impression for a number of these characteristics on the non-verbal level as well. Carol Kinsey Goman, body language expert, tells us in her Forbes article that:

“Research shows that we make eleven crucial decisions about one another – subconsciously evaluating an array of nonverbal cues – within the first seven seconds. And once someone labels you as “likeable” or “un-likeable,” “powerful” or “submissive,” everything else you do will be viewed through that filter”

In addition, Goman lets us know that there are two particular sets of traits are important for CFO’s to communicate non-verbally:

“There are two sets of nonverbal signals that people look for in leaders — status & authority and warmth & empathy — and the most effective leaders employ the right signals at the right time. Which means they realize that the body language signals that work so well when announcing a new business strategy are not helpful (and in fact may sabotage their efforts) when building collaborative teams.”

Recurring themes (the star in our triangulation picture) throughout this post center primarily on relationships and communication. Whether it is the CEO, investors, knowledge experts, service providers, or organizational teammates, making the most of these relationships is essential to CFO success.

Strong communication skills are also required in all the settings. The CFO needs to help investors understand the business while simultaneously convincing them that they are competent to be in the role. Communication with service providers creates a positive working relationship that allows the CFO to utilize these experts productively. Those within the organization need to see the leader's strength, confidence, and conviction.

Within these broad characteristics, the CFO must be versatile in balancing the tactical aspects of relationships and communication, since managing the different groups requires somewhat different styles of interaction. The relationship style with the CEO needs to be open and candid, while with others in the organization the CFO must practice more impression management. With outside experts, the CFO needs to be intimiate enough with their advisors to be able to benefit from their expertise. In all these circumstances, however, it appears they must exude Executive presence, the combination of signals to others that they are a person of status, authority, and expertise.

Note: There is a large body of knowledge about CFOs and what characteristics are considered important. This post will be updated periodically as I run across other items that will contribute to our triangulation approach to the topic.

- ::What are the most important CFO qualities from your perspective?

- ::What experiences have you had with CFOs who did not exhibit strong relationship and communication skills?

Add to the discussion with your thoughts, comments, questions and feedback! Please share Treasury Café with others. Thank you!

Very good, deep post, David. Much for me to digest here. Thank you for writing it. ~Mike

ReplyDeleteThank you Mike. It was a lot for me to digest as well!

DeleteThis was a great post! It had great substance and proposed many points that might often be overlooked. I loved how you broke down point and went into the depth of them. Very well said overall.

ReplyDeleteTailar McCarns

www.mbsaccountancy.com

Thank You and I have a super offer you: How To Plan House Renovation remodel renovation

ReplyDelete